Residential

How to increase your CIBIL Score for Home Loan application

July 24, 2017

Owning a house is every family's dream and a home loan can be a facilitator to make your dream come true. But there are a variety of factors that play an important role in ensuring your application is approved - the most important being your CIBIL Score.

The CIBIL score, also known as the Credit Information Bureau (India) Limited Score or credit score, is a score assigned to a person based on their credit history. You can maintain a good CIBIL score by paying your dues on time and avoiding any late-payment fee.

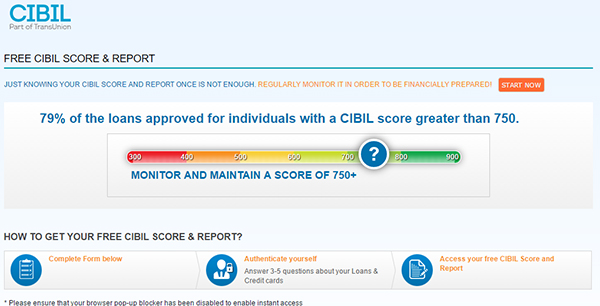

What is a good CIBIL Score?

- Above 750: Excellent credit

- 700 to 750: Good credit

- 600 to 700: Average credit

- Below 600: Low credit

Most loan applications are rejected due to a poor CIBIL score as this score can single-handedly make or break the deal. Read on for a few useful tips on how to increase your CIBIL score and invest in the house of your dreams:

Pay your dues on time

As redundant as it may sound, paying your dues on time and staying wary of late-payment fees is the key to an excellent CIBIL score. It is a good idea to automate your payments, so the dues are paid even before you begin your monthly expenses.

Check your outstanding credits

Since your CIBIL score represents the uniformity in which you have been paying your outstanding dues, it only makes sense to check if you have any pending credits to address. Observe the pattern in which you have been making payments and try regularising it to improve your score.

Build enough credit history

If you haven’t taken a loan in the past or used a credit card, there are chances that you would have very less credit track record - in that case it is recommended to apply for a credit card and use it judiciously with timely payment. This would allow you to build a good credit history.

If your score is low, it is probably because you haven’t been making your payments on time. Now that you have narrowed down to the root of the problem, make sure you settle your dues regularly and watch your score improve over a period of time.

Educate yourself on the type of loan taken

Primarily, all loans fall into two broad categories – secured loans and unsecured loans. Secured loans are high-end loans like home loans or car loans which, when paid on time, contribute to a solid CIBIL score. On the other hand, unsecured loans, are the loans which do not need any collateral, like personal loans or credit cards. The more unsecured loans you have outstanding, the lower your CIBIL score.

Use your credit card wisely:

Monitor your credit card usage very closely as it can easily have a negative impact on your CIBIL score. Make sure you spend within the credit limit provided. For example, if your credit limit is Rs 20,000 and you have an urgent expense of Rs 30,000 coming up, approach your bank to extend the limit. Additionally, make sure you pay back the credit by the due date to avoid interest and late-payment charges.

Don't apply for too many loans

The more loans you have applied for, the higher the probability of a weak CIBIL score. Space out your loans and credit card applications. Apply for a loan only when there is absolutely no other option left and try staying as much in your credit limit as possible. Also, if your loan has been rejected once, work on increasing your CIBIL score rather than approaching other banks as it will only get rejected again.

Check your score regularly

Keeping track of your score is essential as it would give you an idea as to where you stand. You can check your credit score by logging into CIBIL’s official website and following a simple and quick online procedure with a nominal fee. First, you need to fill in your basic information like name, address and income with an identity proof. Then, you will be directed to the payments page where a nominal fee is to be paid, following which you will have to submit authentication details. Once this is done, your CIBIL score will be sent to your email within 24 hours. It is a good practice to keep track of your credit score at least two to three times a year. In case of any discrepancies, approach your bank for clarification immediately.

Increasing your CIBIL score is the only way you can get your home loan approved. Follow our above-mentioned foolproof methods of strengthening your score and watch your dream of owning a house flourish into a full-fledged reality.

Photo credit: investdunia.com

MUST READ

Looking for something specific?

We'd be delighted to help you.